Unfortunately, most professional historical research has become the essentially worthless appendage of Woke ideology. Empirically grounded research focusing on change over time, however, can provide policymakers with important insights, if only they are astute enough to pay attention.

If new policymakers come into office in 2025, they may decide it is in the best interest of the American people to begin dismantling the administrative state, those hundreds of federal government bureaucracies that can diminish, or even ruin, the lives and livelihoods of individual Americans with administrative rules and even poorly conceived and ambiguously worded “guidance” of their own concoction. Before the process of rolling back the administrative state can commence in earnest, though, understanding the problems it currently causes will be necessary, but so too will be understanding how Leviathan came to grow to such proportions in the first place.

My recent trip to the National Archives and Records Administration in College Park, Maryland (NARA II, as it’s known) to view some records at the Securities and Exchange Commission (SEC) highlights both the current condition of Washington’s Deep State swamp and how it acquired its murky depths.

The trip required over a year of preparation. First, my coauthor and I had to file Freedom of Information Act (FOIA) requests with the SEC, for which we had to pay, even though our request clearly established that (as academic researchers writing a research article that could improve public administration) we are legally exempt from its fees. So we filed an appeal. Rather than allow us to win our appeal on the merits, the SEC provided us with 123 box numbers, effectively said “good luck with that,” and mooted our appeal. In response to another FOIA request, it said that because it didn’t respond to our appeal within the time allowed by statute, we were entitled to a fee waiver but in order to respond to our request, it needed just a little bit more information. It then proceeded to ask us for the very information that we had asked of it.

Clearly, the SEC did not want to set a precedent by granting that our research met the criteria for a fee waiver. And given that my coauthor and I had published a high-profile journal article establishing its complicity in the 2008 global financial crisis, the SEC did not feel the need to be overly helpful with our new study, which could prove that a staff member twisted one of the SEC’s rules to protect racial segregation in the postwar South.

The Kafka-esque nature of NARA II then revealed itself. We appeared with the 123 box numbers only to be informed that we had to also submit a FOIA to the National Archives before we could see some of the boxes. Yes, we had to file a Freedom of Information Act request with the part of the federal government devoted to sharing information about the federal government with the public! You know, because [insert your favorite administrative word salad here]. That was when we learned that, of the 123 boxes referenced by the SEC, only nine still exist. Thankfully, they were big boxes.

We then had to wait while the boxes were screened, how or for what material we do not know. The SEC’s records are in such utter disarray that I would not have been surprised to pull out a dead possum, but thankfully the nine boxes housed tens of thousands of miscellaneous memoranda, forms, and letters in roughly chronological order.

Physical and psychological barriers abound at NARA II. The staff were always friendly, and thankfully they did not arrest me for inadvertently breaking their protocols on several occasions. Checkpoints and obstructions rule the building and its visitors: Show the guard your drivers’ license when you drive up, go through a TSA-like security checkpoint, sign in (if your name was on the list generated by reserving a spot weeks in advance), get a registration card, drop your stuff off in lockers in the basement, go back up to the lobby level to join the queue, scan the QR code on your registration card, prove (again) that your laptop is a laptop and not a document theft device, take the elevator to the reading room, scan in again there, put in your call slips if you are lucky enough to have some, wait and wait and wait for your name to appear on an airport-like monitor, get your boxes, take them to another desk 50 yards away to get a permission slip to take pictures of the documents, and then, finally, begin work. Pray, though, that you don’t find an interesting document bound by a staple or clip, lest more hoops be summoned for the researcher to jump through.

More screenings and scans were needed to exit. This was all done to protect the precious files from damage or theft. A most wanted poster outside the reading room door warned all to watch out for known document thieves! For reasons no one could explain, though, the poster did not mention Joseph Biden or Donald Trump.

Despite all those barriers, or because of the disorganized nature of the files, we were able to find what we were looking for, plus a whole lot more, and not a single mummified possum.

As I reported in my 2019 AIER book Financial Exclusion, women were active in the securities markets by the 1930s, as (disgruntled) investors and by the 1950s as trouble-making brokers, like Winifred Rose Galbraith and Margaret A. Sweeney, who perpetrated heinous crimes like not filing Rule X-17A-5 or Section 15(b) paperwork for a few years. Mrs. Anna F. Ross, doing business as Moore & Company out of Jersey City, got pinged in 1951 for employing procedures that the SEC claimed did not “adequately safeguard the interests of customers.” It gave her 40 days to shape up or face legal consequences.

Women also ran into legal difficulties with the SEC when they acted as influencers for bad actors. In 1944, for example, a beauty parlor operator named Mrs. Von Martinitz lured her clients and friends into the iniquitous den of oil lease shyster Harvey G. Martin. Both consented to a permanent injunction.

One of the SEC’s first key staffers was Miss Olga M. Steig, a published Progressive with experience in Wisconsin’s Blue-Sky securities law bureaucracy. She joined the SEC and quickly rose through its ranks to become Supervisor of the Broker-Dealer section by 1937 and by 1943, Assistant Director of the Trading and Exchanges Division, a post she held for over a decade.

Most of the SEC’s female employees, though, were clerical staff – secretaries, stenographers, and the like. At least one engaged in a work slowdown when denied a reclassification and salary increase, during the Roosevelt Depression of 1937 no less. When another began to complain about her compensation, she was immediately promoted and her salary raised to $2,000 per year, considerably more than the average Texan then made. The SEC brass could not afford to lose her because she worked until 6 pm when needed. Now that’s dedication.

Most importantly, perhaps, the archives reveal how the SEC managed to grow over the years, despite considerable initial opposition against it.

First, the SEC ran an active PR campaign to induce newspapers to write nice things about it. Information officers like William T. Raymond made sure to send reports and releases to key people in the media, while staffers scrutinized the filing forms of unfriendly papers, like those of William Randolph Hearst. The results of its “carrot and stick” approach were palpable and generally positive. On 27 February 1946, for example, the Philadelphia Evening Bulletin ran a puff piece extolling the Commission’s work and arguing that “it would be a penny-wise, pound-foolish policy to cut down” its budget because it “faithfully carried out the policy which President Roosevelt set for it – to make the seller as well as the buyer of securities beware,” as if fraud laws had not existed prior to the New Deal.

The SEC also took partial credit for winning World War II, because without its protections, it claimed, investors would not have had enough confidence to buy corporate stocks or bonds. It turned its own tenth annual report into a paean to its heroic history and then sent it to every major media, business, and political figure it could think of, garnering itself “attaboy” replies from astute utilities executives, and even President Truman himself.

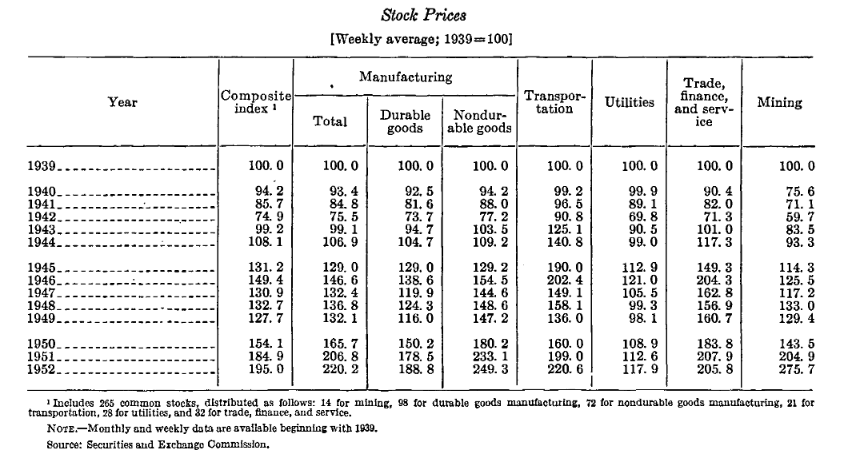

Relatedly, the SEC provided individuals with statistical information at no charge. That included a stock market index in no way analytically superior to those of Dow Jones or other private entities, except that it appeared “free” to the people consuming it.

Second, the SEC required securities issuers, brokers, and exchanges to come to it for permission on numerous niggling matters, like permission to mail proxy solicitations earlier than it normally allowed, or to keep executive salary information confidential. It quickly doled out such minor favors to complacent companies while ignoring or denying the requests of problematic firms on flimsy pretexts. Monitoring such minor details drained the SEC’s resources but increased its power by inducing companies to stay on its good side by rapidly complying with its dictates.

The SEC also rewarded corporate complicity by not pushing for reforms that would have proven personally embarrassing or costly for executives. Although it collected salary information, it did not publish the results, forcing individuals to inspect filings if they wanted to know how much the top executives made, and only then when the SEC did not consent to keep the numbers confidential. It also did not try to return to stricter governance regimes, including one desired by stockholders who wanted directors to own substantial amounts of stock in the companies they led. Instead, the SEC put the onus on individual stockholders, most of whom had neither the time nor the expertise to challenge fundamental corporate policies.

Third, the SEC always claimed to be doing the best job it possibly could with its ever-meager resources. Its solution to every problem was a bigger budget, not cutting its costly “free” information or PR programs, nor streamlining its clumsy administrative structure. Its Chairman, Jerome N. Frank, panicked in 1940 when he feared the SEC’s budget would be slashed, or its functions turned over to a special wartime agency which, of course, “would not be adequately mindful of the standard for projections of investors.” Its next chairman, Ganson Purcell, counterattacked in 1942 by arguing that corporations were right to complain about their paperwork burden given “the informational requirements of the many interested war agencies.” The SEC, he argued, should be empowered, statutorily and economically, to collect all the necessary information “owing to the experience and training of this Commission’s personnel in the corporate financial field.”

In December 1952, the Heller Subcommittee of the Committee on Interstate and Foreign Commerce in the House of Representatives criticized the way the SEC handled five specific cases. The SEC responded quickly by noting that it provided Heller’s committee with data on 742 cases and that four of the mere five it criticized “involved attacks upon the Commission by private individuals with their own special interests at stake.” As for the other case, “although we disagree with such criticism,” it explained, “we have repeatedly brought to the attention of the Congress the fact that our staff is not large enough for the task assigned to us.” Even with more money, “we could not claim absolute perfection,” but it could get closer to that goal. Unconstrained thinking anyone?

That same year, the SEC split the difference with the American Society of Corporate Secretaries, which argued that the SEC should drop its proposed requirement for quarterly financial reports as impractical, potentially misleading, and creating costs far exceeding the implied benefits for investors. In 1955, the SEC mandated semiannual reporting as a step towards quarterly reporting, which it mandated in 1970. The net effect of quarterly reporting remains debated to this day, but it appears to satiate the government’s need for “legibility” more than it aids investors, in part because it gives management incentives to focus on short-term appearances rather than longer-term realities.

The SEC also attacked self-regulation of the over-the-counter market, claiming in 1951 that self-regulation “cannot ordinarily achieve the high standards of conduct which the Commission, the public and the progressive members of the over-the-counter business consider essential.” It offered no empirical evidence for the claim, which ignored centuries of experience, and proceeded to exert more authority over over-the-counter brokers and dealers.

In short, much of the growth of the SEC can be seen as a variation of the “Baptists and bootleggers” story, where the SEC is the bootlegger earning bigger budgets by combining with people who believe that its nostrums protect investors, even when they do not.

To reverse the growth of the administrative state, America needs laws, rules, incentives, and social mores that require that government actions to be economically rational. In other words, for a rule, regulation, or guidance to remain in effect, the government should have to shoulder the burden of proving that its real-world effects match its rhetorical claims. Moreover, the net effect of the policy on all parties, not just the Baptists and the bootleggers, should be estimated and publicly considered.