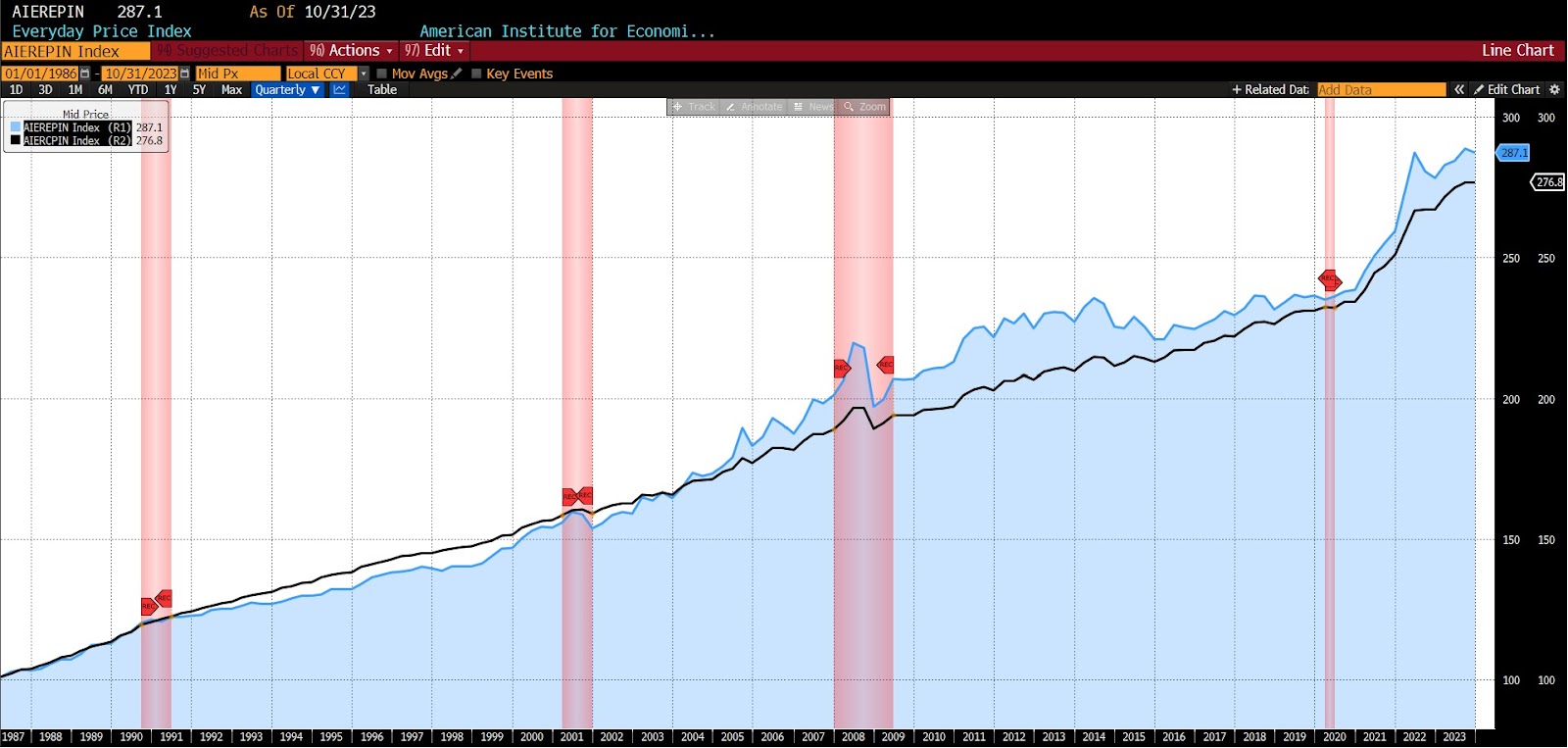

In October 2023 the AIER Everyday Price Index (EPI) fell 0.49 percent to 287.1. This is the second monthly decrease in 2023 (the first came in May 2023), and the largest pullback since the over 1 percent index decline in December 2022.

AIER Everyday Price Index vs. US Consumer Price Index (NSA, 1987 = 100)

Within the EPI the largest monthly increases among constituents came in food at home, food away from home, tobacco and smoking products, and prescription drugs. Price declines were seen in motor fuel, housing fuels and utilities, satellite and live TV streaming, and internet services. Between September and October 2023, the prices of fifteen EPI components rose, one was unchanged, and six fell.

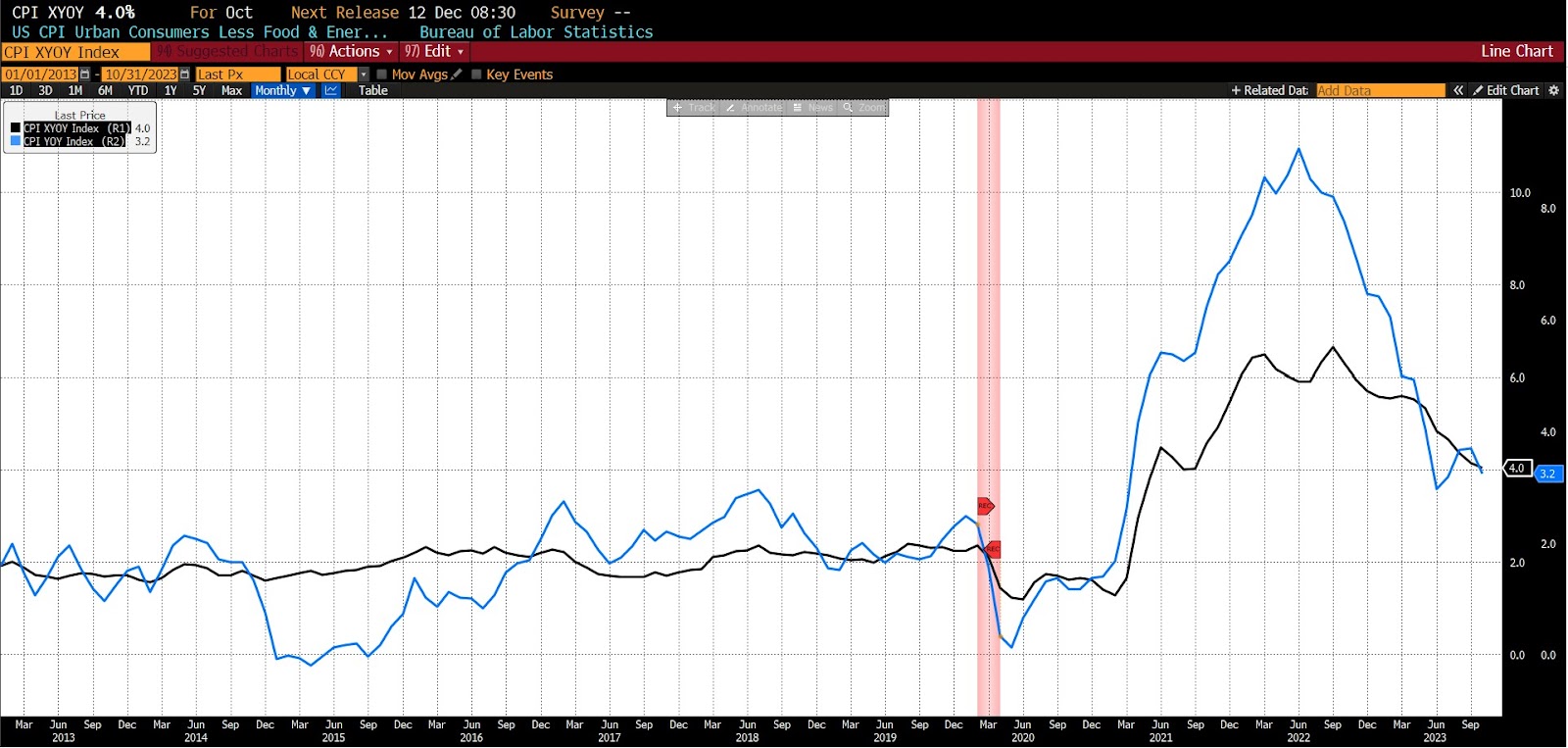

On November 14th the US Bureau of Labor Statistics (BLS) released Consumer Price Index (CPI) data for October 2023. The month-to-month headline CPI number was flat, beating surveys expecting a rise of 0.1 percent. The core month-to-month CPI number rose 0.2 percent, 0.1 less than expectations.

October 2023 US CPI headline & core month-over-month (2013 – present)

While gasoline prices fell in October, they were offset by rising shelter prices. The largest contributors to the month-over-month core index were rent, owners’ equivalent rent, motor vehicle insurance, and medical care. The largest declines from September to October 2023 were lodging away from home, used cars and trucks, communication, and airline fares.

On the year-over-year side, headline CPI rose 3.2 percent versus an expected 3.3 percent. Core CPI (again, year-over-year) rose 4.0 percent versus an expected 4.1 percent. The largest contributors to the year-over-year October 2022 to October 2023 changes were shelter (which accounted for 70 percent of that increase), motor vehicle insurance, and recreation. Declining substantially on a year-over-year basis were prices of household furnishings and new vehicles.

October 2023 US CPI headline & core year-over-year (2013 – present)

The October CPI numbers were the first in some time to deliver a surprise on the downside. Annualized core CPI is running at 2.8 percent on a one month basis, 3.4 percent on a three month basis, and 3.2 percent on a six month basis, down from September readings of 3.9 percent, 3.1 percent, and 3.6 percent respectively.

Broad moderation in inflation measures to levels generally consistent with the Fed’s objectives resulted in a rapid repricing of Fed Fund futures early in the session. The market implied chance of another Fed hike before the end of 2023 dropped to less than 10 percent. Additionally cited as positive in the October report was the growing diffusion of disinflation among CPI constituents, with the percent of core spending items showing declining prices rising to 41 percent from 33 percent in September. Additionally, the share of core prices for which annualized prices rose at a rate of above 4 percent fell from 44 percent in September to 38 percent in October.

The October inflation release provides a welcome respite from resurgent price increases over the past few months. Beyond the consumer perspective, the suggestion that policy rates may be at their peak is undoubtedly good news for upcoming budget negotiations, a central focus of which has been surging US Treasury yields and consequently increasingly unsustainable debt service costs. Nevertheless: while the most recent CPI (and EPI) data relay a positive state of affairs in the resumption of the disinflationary trend, it is essential to emphasize that challenges and uncertainties persist.