According to new a research report from the IoT analyst firm Berg Insight, the installed base of water utility AMI endpoints in Europe and North America is set to more than double during the period 2022–2028.

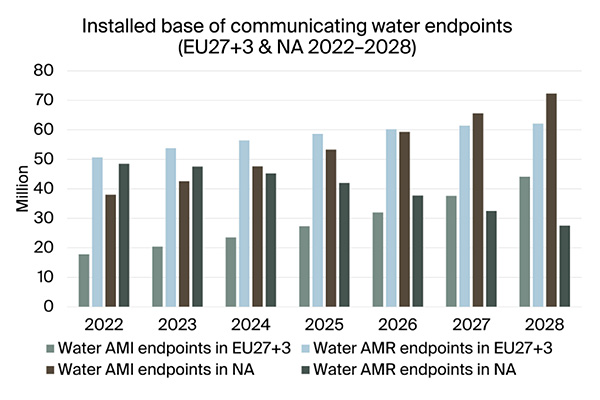

At the end of 2022, the combined installed base of AMI endpoints in Europe and North America amounted to 55.8 million units. This number is expected to grow at a CAGR of 13.0 percent to reach 116.4 million in 2028. The total number of communicating utility water meters – including both AMI and AMR – will at the same time grow from 155.1 million units in 2022 to 206.0 million units in 2028.

AMR includes metering points that require readings through drive-by or walk-by operations while AMI involves a fixed network communications infrastructure and supports true IoT connectivity.

“Since the Covid-19 pandemic, the growth of remote water meter reading technologies has been impeded by supply-chain disruptions, resulting in the postponement of several projects. With ongoing improvements in supply-chains coupled with significant commitment from numerous utilities to implement smart metering technologies, the outlook for the overall smart water metering market looks promising”, said Mattias Carlsson, IoT Analyst Berg Insight.

In terms of AMI connectivity, LoRaWAN and 3GPP-based LPWA technologies such as NB-IoT and LTE-M continue to be the fastest growing technology types for new water AMI deployments in Europe and North America.

In Europe, Spain has emerged as the leading European adopter of 3GPP-based LPWA communications for water AMI with several major utilities in the country now launching large-scale rollouts based on NB-IoT. The interest in 3GPP-based LPWA is also particularly strong in markets such as the UK, Italy and the Baltics while demand for LoRaWAN has so far been more widespread across the entire European region.

In North America, LTE-M currently constitutes the single fastest growing technology for new water AMI deployments while LoRaWAN has just started showing some growth after several years in the market.

“Proprietary and EN 13757-based RF communications technologies currently have a strong footprint in both the European and North American markets. These technologies are anticipated to remain pivotal connectivity options for water AMI projects in the foreseeable future. Nevertheless, emerging alternatives such as LoRaWAN and cellular communications are rapidly growing and are poised to capture a larger share of AMI shipments in the years ahead”, continued Mr. Carlsson.

At the end of 2022, the companies that had accumulated the largest installed bases of water AMI endpoints in Europe included Diehl Metering, Itron, Birdz (Veolia), Sensus (Xylem) and Kamstrup. The top five in North America were Sensus, Badger Meter, Itron, Aclara (Hubbell) and Neptune Technology Group. Top 10 vendors in either of the two regions moreover included the Minol-ZENNER Group, Honeywell, the Arad Group, Mueller Systems, Landis+Gyr, Apator and Maddalena. The SUEZ subsidiary SUEZ Smart Solutions also constitutes a key player in the European water AMI market by having been instrumental to the development and deployment of Wize technology.

The post Water AMI landscape 2028: Exceeding expectations with over 100 percent growth in Europe and North America appeared first on IoT Business News.