As the S&P 500 and Nasdaq 100 once again test new all-time highs this week, I’m struck by how leadership trends have shifted around quite a bit since mid-December. Part of my daily chart process involves a series of ratios to better evaluate and understand which stocks are leading, which stocks are lagging, and from where the next big leadership theme may emerge.

Here are three key ratio charts that I’ve found incredibly valuable in recent years, all derived from my Market Misbehavior LIVE ChartList. I should also note that the Relative Rotation Graphs remain one of my primary tools to track leadership rotation among the 11 S&P 500 sectors. I feel that the charts below complement the RRG to provide a more comprehensive picture of rotation among themes and styles.

This first chart hits on perhaps the most important equity market theme in 2024, the dominance of growth over value. The top panel compares the Russell 1000 Growth vs. Russell 1000 Value ETFs, which pulled back into mid-January before rallying again this week.

Next we have the S&P 500 Pure Growth and Value ETFs, which ignore stocks like Microsoft Corp. (MSFT) that are “double counted” as they display both growth and value characteristics. This chart has once again broken to new highs as growth stocks have spiked higher this week.

Finally, we’re charting a ratio of the S&P 500 High Beta and Low Volatility ETFs, which has been steadily trending higher since early September. This provides another way to demonstrate how higher beta companies, or those that tend to experience stronger movements than the benchmark, have done better than more conservative names that tend to demonstrate less volatility than the benchmark.

Even though strategists, including yours truly, have been speaking of the “return of small caps” for quite some time, this next chart shows that investors are still waiting for that fateful day to arrive. The Russell 2000 ETF has been underperforming its large cap counterpart fairly consistently over the last two years, and the equal-weighted S&P 500 ETF is close to a new 52-week low relative to the regular cap-weighted S&P 500 ETF.

While conditions appear to be ripe for small caps to outperform, these ratios show how the strength in large caps continues to be a key market theme. Indeed, for the last 12 months, owning anything but large cap growth stocks most likely did not help your portfolio, with the notable exception of a rare few outperformers. When in doubt, follow the trend. And the trend remains favoring large cap stocks.

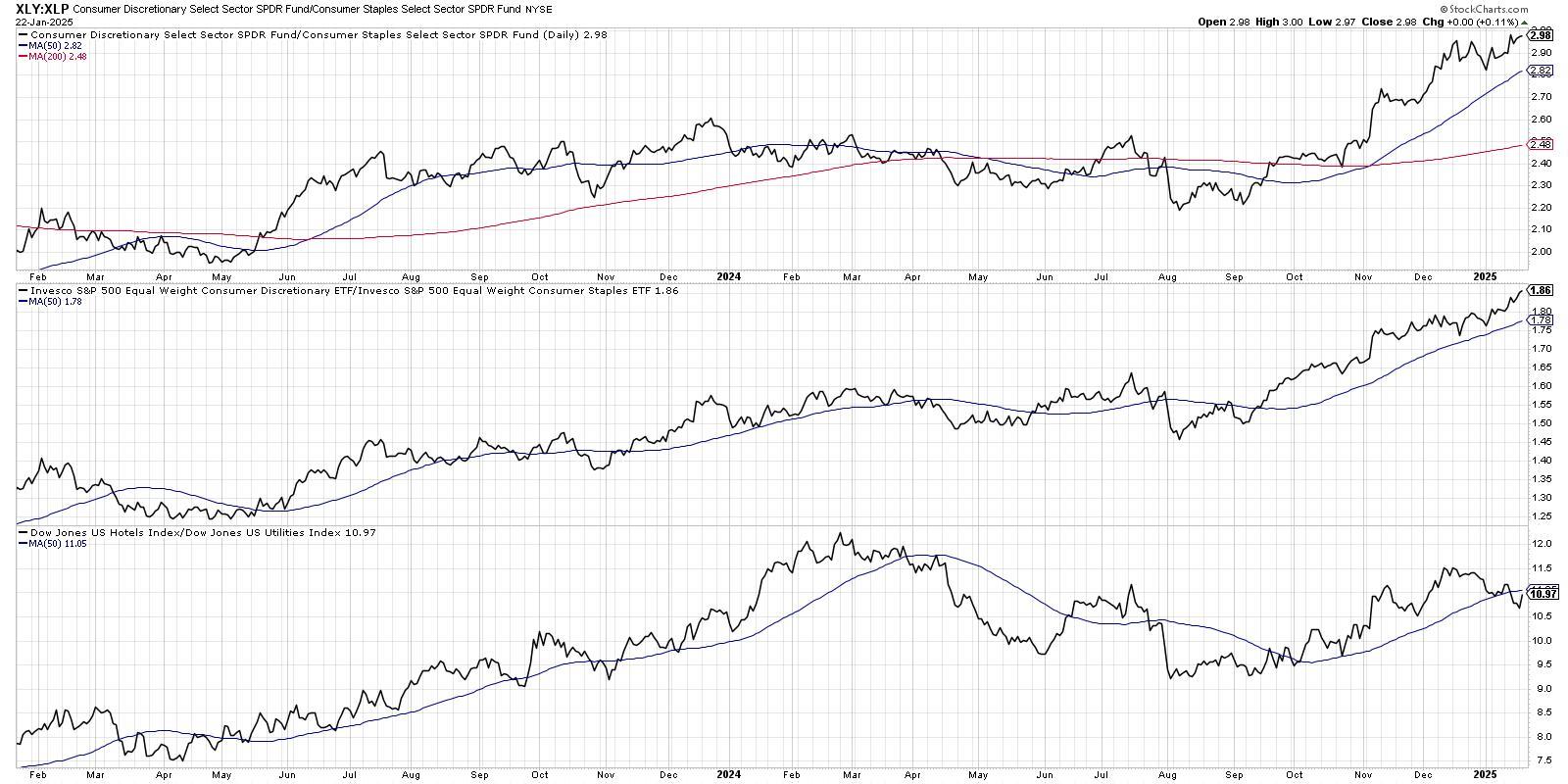

These next three data series represent what I call “offense vs. defense”, in that they track traditionally offensive sectors like consumer discretionary vs. traditionally defensive sectors like real estate. With the exception of the bottom data series, showing how hotels have underperformed utilities, this chart shows that investors are still favoring “things you want” over “things you need”.

To put it another way, offense is still winning over defense.

Overall, despite a clearly corrective move at year-end 2024 into early 2025, these equity markets appear to have rotated right back to a growth-led bull market phase. By consistently reviewing the charts we’ve discussed above, you should be able to better identify shifts in leadership and hopefully take action to better position yourself for what may come next.

For two more bonus ratio charts covering key asset allocation themes, be sure to check out my latest video on the StockCharts TV YouTube channel!

RR#6,

Dave

PS- Ready to upgrade your investment process? Check out my free behavioral investing course!

David Keller, CMT

President and Chief Strategist

Sierra Alpha Research LLC

Disclaimer: This blog is for educational purposes only and should not be construed as financial advice. The ideas and strategies should never be used without first assessing your own personal and financial situation, or without consulting a financial professional.

The author does not have a position in mentioned securities at the time of publication. Any opinions expressed herein are solely those of the author and do not in any way represent the views or opinions of any other person or entity.