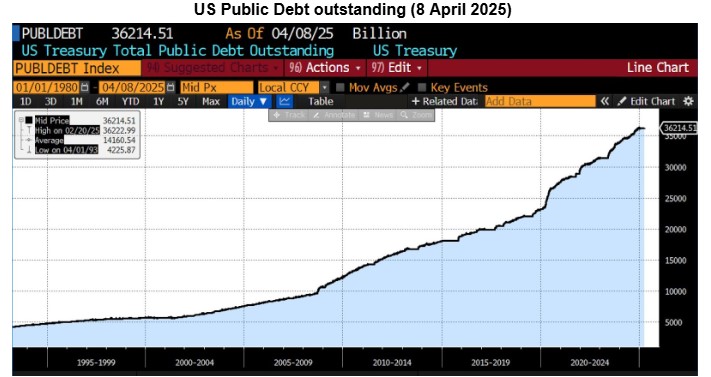

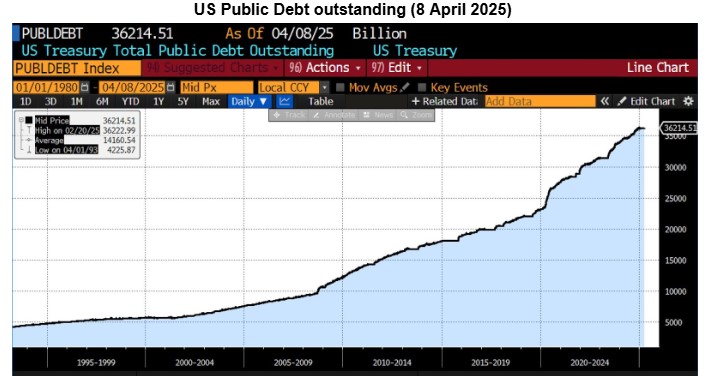

In times of rising debt and fiscal strain, unconventional ideas occasionally surface as ways to manage the US government’s borrowing obligations. Few have forgotten the trillion-dollar platinum coin scheme a few years back. A recent suggestion, associated with Stephen Miran’s A User’s Guide to Restructuring the Global Trading System (a.k.a. The Mar-a-Lago Accord) involves forcing or pressuring holders of US Treasury securities to exchange their current bonds—many with short- or medium-term maturities—for 100-year bonds carrying lower interest rates.

On the surface, the plan seems attractive: it could reduce short-term debt servicing costs and push out repayment far into the future. However, viewed through legal, financial, and market lenses, the plan is a nonstarter—at best unrealistic, and if pursued, potentially disastrous.

Below are seven key reasons why such a strategy would be unworkable and harmful to the credibility of the US government and the functioning of global financial markets.

1. It represents a violation of the contractual terms

Treasury securities are formal contracts between the US government and investors. They specify the amount borrowed, the coupon rate, and the repayment date. Investors buy these securities with the legally binding expectation that the terms will be honored. A forced conversion into 100-year bonds—particularly those with lower yields—would represent a breach of contract. This would likely result in a wave of legal challenges in US courts and could be interpreted as a selective default by credit rating agencies. More broadly, it would send a chilling message to investors that the US government cannot be relied upon to meet its obligations under previously agreed terms. That reputational damage would have lasting consequences for the government’s ability to borrow in the future.

2. Dumping or another form of retaliation is likely

Foreign governments and central banks are among the holders of US Treasury securities, holding trillions of dollars’ worth as part of their currency reserves and financial stabilization strategies. If these entities were forced to exchange their existing holdings for ultra-long-term, lower-yielding bonds, they might interpret it as an act of bad faith or even financial expropriation. In response, some could retaliate economically or strategically, but most would likely begin to liquidate their Treasury holdings—either to avoid further exposure or as a form of protest. A coordinated or large-scale selloff by foreign holders would depress bond prices, push yields higher, and potentially weaken the dollar. The resulting financial instability would erode the US government’s long-standing position as the issuer of the world’s reserve currency.

3. There are considerable legal and political obstacles

Any plan to convert existing Treasury debt into 100-year bonds would encounter immense legal and political resistance. Congress would likely need to pass enabling legislation, and bipartisan opposition would be fierce, likely citing both the Contract Clause and the Takings Clause. Lawmakers across the ideological spectrum would view the measure as a direct threat to the full faith and credit of the United States. Moreover, contract law strongly protects the rights of bondholders, and retroactively changing debt terms would almost certainly be challenged in court. The only conceivable workaround—invoking emergency executive powers—would trigger a constitutional crisis and further erode domestic and international trust in US governance. The political fallout would be severe, and the financial markets would respond accordingly.

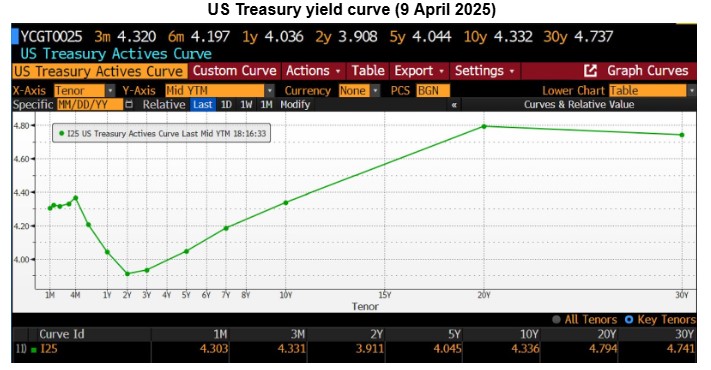

4. 100-year bonds with low yields are an unlikely and unattractive outcome

From a financial perspective, longer-term bonds carry substantially more risk than shorter-term ones. Investors exposed to longer maturities face greater uncertainty over inflation, interest rates, and creditworthiness. As a result, markets demand higher, not lower, yields for longer-term bonds. Forcing or even encouraging investors to accept lower-yielding 100-year bonds in exchange for their existing securities contradicts this basic principle of finance. The scale of this mismatch is glaring: a 1-year Treasury converted into a 100-year bond represents a 100-fold increase in maturity; even a 30-year bondholder would be tripling their time exposure. Yet the plan proposes that these investors accept lower compensation for that additional risk—a proposition that defies economic logic.

Further complicating matters are the bond market dynamics of duration and convexity. Duration measures how sensitive a bond’s price is to changes in interest rates. A bond with high duration—like a 100-year bond—will see its price fall significantly if interest rates rise even modestly. Convexity, which describes how a bond’s duration changes as interest rates move, becomes more pronounced in ultra-long bonds. While convexity can help slightly in very large interest rate swings, it also introduces greater pricing volatility and uncertainty, making 100-year bonds particularly hard to hedge or model. For many investors—especially those with liability-matching needs or regulatory constraints—this makes such instruments unappealing or outright unmanageable.

Finally, these ultra-long bonds would be less useful as collateral in the banking system. Treasury securities are widely used in repo markets and other secured lending arrangements because of their liquidity and relatively stable pricing. But the longer the maturity, the more volatile the market value—meaning that 100-year bonds would need to be deeply discounted (with a higher “haircut”) when used as collateral. This reduces their effective value in day-to-day financial operations and makes them a poor substitute for the shorter- and medium-term Treasuries currently in wide circulation. Additionally, their low liquidity and lack of historical issuance would make them harder to price and trade efficiently, further diminishing their utility in modern financial systems.

5. It would set a negative precedent and ratchet up moral hazard

The long-term consequences of forcing a debt restructuring would extend beyond the immediate market shock. If the US government sets the precedent that it can change repayment terms unilaterally—even in pursuit of efficiency or cost savings—it opens the door to future manipulations. Investors would begin to price in the risk that terms might change again under future administrations or during future crises. This creates a “moral hazard” problem where the government is seen as an unreliable borrower, ultimately raising borrowing costs and damaging its credit rating. More broadly, such a move could encourage other indebted nations to follow suit, weakening the integrity of sovereign debt markets globally. For a country that issues the world’s reserve currency and whose bonds underpin the global financial system, the risks of setting such a precedent are especially grave.

6. Maturity stretching solves no fiscal ill

Even if the market accepted a swap of shorter-term debt for 100-year bonds—at appropriately higher yields to reflect the vastly longer exposure—such a maneuver would do nothing to resolve the underlying structural fiscal imbalance. It would merely change the timing of repayments, not their scale or structure. The central issue is not the maturity profile of US debt, but the chronic mismatch between government spending and revenue. As long as deficits persist—year after year—the total debt will continue to rise regardless of how it is financed. The debt problem will only be addressed when the deficit problem is resolved. That means aligning federal spending more closely with tax revenues through either fiscal consolidation, revenue increases, or both. Until that occurs, restructuring debt maturities is just a cosmetic change, not a real solution.

7. It could lead to a loss of confidence and market panic

Investor confidence is the cornerstone of stable financial markets, and US Treasury bonds are the global benchmark for low-risk assets precisely because of their reliability and predictability. If the government were to unilaterally alter the terms of its debt—extending maturities and lowering yields—investors would perceive this as a form of financial coercion or soft default. Such a move would spark a massive selloff in Treasury markets, drive up yields across the curve, and destabilize global portfolios that rely on Treasuries as a safe store of value. Broader market volatility would likely follow, including sharp declines in equities and liquidity freezes in credit markets. The ripple effects could extend to emerging market economies, corporate bond markets, and even the real economy through higher borrowing costs.

While the idea of reducing interest costs by converting existing debt into ultra-long, low-yielding bonds might sound like a creative solution to America’s debt challenges, it fails every test of financial realism, legal integrity, and political viability. It would violate contracts, damage the United States’ reputation as a trustworthy borrower, shake global confidence, reduce the usefulness of Treasuries in collateral markets, and set a damaging precedent for fiscal governance. Worse, even if done at market-clearing interest rates, it would not address the structural driver of debt growth: persistent federal deficits. Rather than stabilizing public finances, such a move would almost certainly ignite a full-blown financial crisis. In a world that still (and somehow inexplicably) depends on US debt markets, tampering with that foundation carries more risk than reward.