Ronald Reagan deserves much praise for his stalwart commitment to free trade and lowering trade barriers.

Even his most contentious policy—the Voluntary Export Restraint (VER) agreement with Japan—can be seen as a defense of free trade, once the context and Reagan’s limited options are understood.

But was the VER agreement a success?

Do Trade Restrictions Fuel Growth?

New Right thinkers such as Oren Cass certainly seem to think so, claiming two successes from Reagan’s non-policy: the VERs caused domestic job growth in manufacturing and increased foreign investment in the US. This is an important distinction and is crucial to his argument. He is asserting that both the manufacturing job growth and the foreign investment would not have happened without the VERs. He then alleges that these results can and will be replicated under a sensible tariff regime.

The effect of the VERs on job growth was, indeed, initially quite positive. A 1985 International Trade Commission report says that “it is likely that the [VER] added about 5,400 jobs to US automobile employment in 1981, and by 1984, the [VER] was responsible for a total of 44,000 additional jobs in the domestic industry.” And to be completely fair, the report goes on to say that “If the employment gains in the steel industry and in other supplier industries were added to these numbers, the gains in employment would be significantly higher.”

Frankly, this is unsurprising to anyone who has even a cursory understanding of economics. No economist denies that, in the short run, employment effects of protectionist policies can be quite positive. This is, in part, thanks to long-term contracts that firms across supply chains have with one another. With little time to adjust to price changes (a concept economists refer to as “elasticity”), producers have little choice but to accept the higher prices. The Second Law of Demand teaches us that elasticity changes over time, specifically that when a higher price persists for a long time, purchasers will have more time to find adjustments to this new price, which will exacerbate the diminishment in purchases caused by the higher prices to begin with.

As an example of this, consider aluminum. When faced with higher prices due to the tariffs placed by the first Trump administration, many aluminum canning operators reduced their purchases of aluminum and produced fewer cans. Due to the decreased production of cans, canning operations laid off workers. But over time, as the availability of alternatives increased, production processes for industries reliant on aluminum cans changed. Craft breweries, for example, shifted away from selling their beer in six packs of smaller cans and toward four packs of taller cans containing the same volume of beer. In doing so, they were able to massively reduce the amount of aluminum used by volume of beer. Likewise, some are considering switching to glass bottles instead, which would eliminate their purchases of aluminum entirely. As sales of aluminum fall, so too does employment in the aluminum producing sector. The tariffs, which were intended to protect the domestic aluminum industry, are actually having the opposite effect in the very industry they were intended to protect. Strangely enough, it would appear that the pandemic (of all things) is responsible for the aluminum-producing sector’s resurgence, not tariffs.

Just as with other forms of trade restrictions, as a result of the VERs, cars sold in the US — domestically produced or otherwise — all became more expensive. In 1980, Japanese cars were selling for $6,585 while domestic cars were selling for $7,758. In 1986, domestic car prices had increased by 24 percent to $8,229, and Japanese car prices grew by 18 percent to $9,223. These cost increases fell disproportionately on more price-sensitive consumers (lower income households). While “buying a new car” might seem like a luxury, the rise in price for new cars has knock-on effects in the used car market, driving their prices up as well. Further, we should keep in mind that every year, a new group of people look to enter the workforce for the first time, and buying a car may be necessary to do so. More expensive cars make life harder for these people, too.

But were the pains of the higher prices for cars simply a short-term pain that begot long-term gains? Hardly.

The US auto industry, freed from much of the pressures of foreign competition squandered the opportunity to move away from the midsize and large car options they had been producing and toward the smaller, less expensive, and more fuel-efficient cars like those made by Japanese automakers. Oil shocks in 1973 and 1979 and a recession in 1980 and 1981 moved US consumers away from wanting larger, less fuel-efficient cars, toward smaller, more fuel-efficient cars, which was exactly what the Japanese automakers were selling in the US. In addition to being cheaper and more fuel efficient than American cars, Japanese cars in 1980 also required far fewer repairs. By 1990, Japanese cars still required fewer repairs, and the gap in quality had grown wider. Again, this makes sense to an economist: the sting of losses is a powerful force that drives innovation. By reducing this sting in the domestic auto industry, the VERs reduced the need for innovation in the domestic auto industry. Japanese car makers, by contrast, shifted their exports away from lower quality cars and toward higher quality cars. Economist Robert Feenstra demonstrates that two-thirds of the increased price of Japanese cars after the VER took effect was due, in fact, to improved quality of Japanese imported cars.

As a result of this, in the 1990s, the Big Three automakers — Ford, General Motors, and Chrysler (now Stellantis) — were forced to lay off tens of thousands of workers. In fact, January of 1990, the LA Times reported that “a staggering 42 of the 62 Big Three Assembly plants are being shuttered at least temporarily during January.” If anything, the short term pains of higher prices for consumers led to the long term pains of reduced employment for workers.

In fact, the Big Three did not even want the import restrictions to begin with. Doug Irwin writes, “GM, Ford, and Chrysler did not want to restrict imports because they themselves had begun importing foreign produced cars under their own nameplate. In 1975, the UAW charged twenty-eight foreign auto manufacturers in eight countries with dumping, but domestic producers did not support the petition because 40 percent of imported cars came from their subsidiaries.”

But what about the increased foreign investment, particularly in the American South? Surely, while Detroit struggled, carmakers like Honda and Toyota, who started to build plants in the US and thus avoid the export restraint restrictions, right?

Wrong.

First, it would be silly to imagine that a temporary, voluntary restraint on exporting goods into the US would impel Japanese auto firms to invest millions of dollars into building assembly plants and the necessary infrastructure to make these plants operational.

Volkswagen began building manufacturing plants in Pennsylvania in 1978 and Honda built its first plant in Ohio in 1979, two years before the VER, building motorcycles. Seeing their successes, Honda then announced more plants being built in 1980, which began opening from 1982 to 1986. Why is this?

According to a 1990 report by the Philadelphia Federal Reserve, Japanese auto firms producing in the US made economic sense. This was not due to the VER, it was because “the production cost differentials between [Japan and the US] have narrowed. One industry analyst has estimated that as of late 1989 an auto can be built at a transplant for $200 less than one built in Japan and delivered in the United States.” At the same time, due to exchange rates and wage rates in Japan, labor was becoming more expensive in Japan relative to the US. In short, rising costs of production in Japan meant that they sought to offshore manufacturing jobs… to the US.

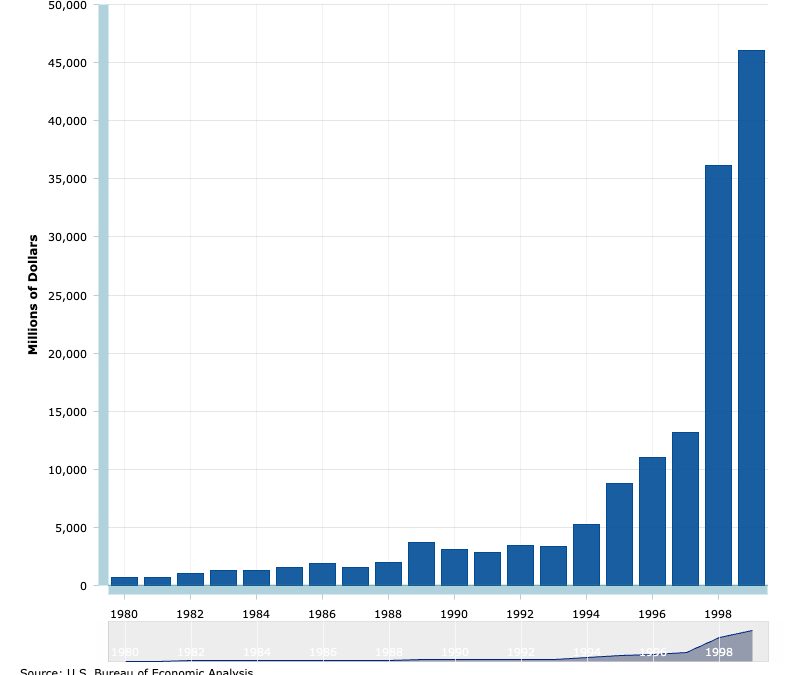

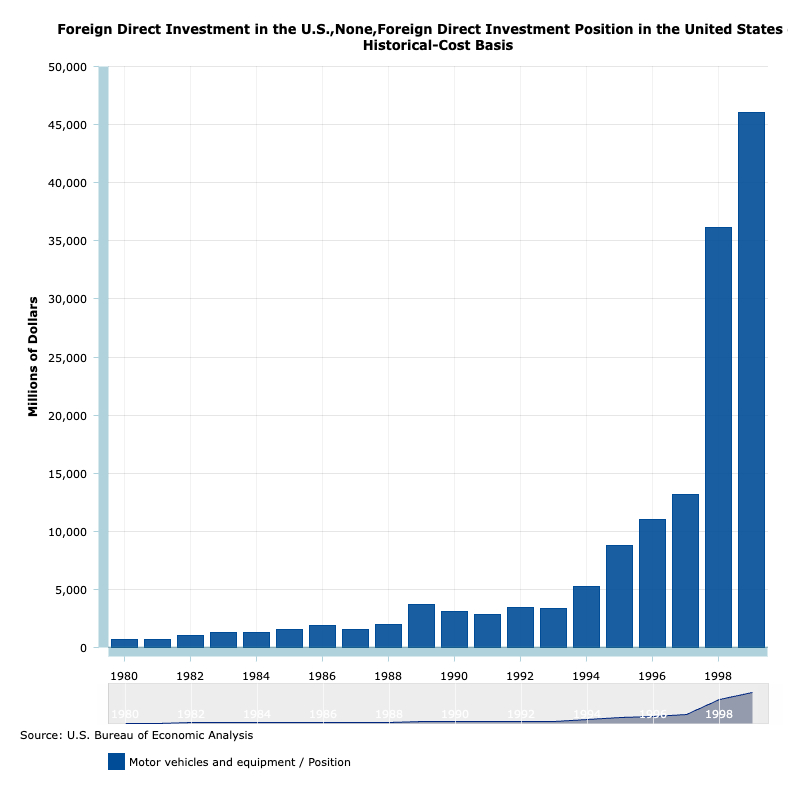

In fact, if we look at the data, we see about $652 million of foreign direct investment in 1981 versus $5.3 billion in 1994 when the VER ended. In other words, a 700 percent increase in foreign investment. That sounds like a lot until we see that from the increase from 1994-1999: a 770 percent increase in just five years as compared to the fourteen years of the VER, increasing foreign investment in the US auto sector from $5.3 billion to a staggering $46.1 billion.

If anything, what this suggests is that it was trade liberalization, not protectionism, that spurred foreign investment. But what about more recent times?

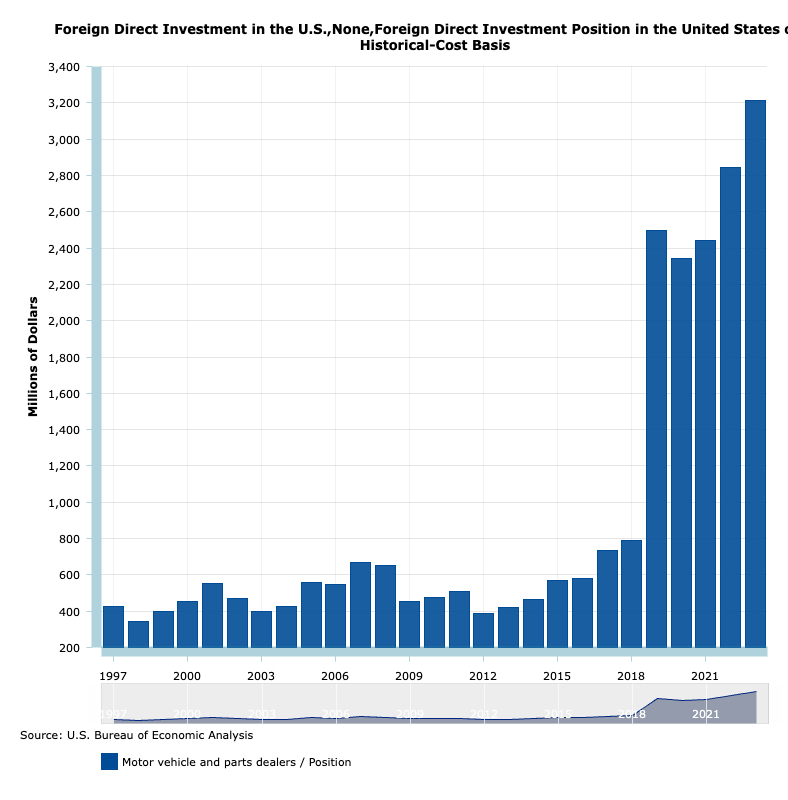

There was indeed a marked increase in foreign direct investment in 2019; in fact, it more than tripled and remained significantly elevated through 2024. There is a certain argument to be made that at least the initial increase in foreign direct investment in 2019 was caused by Trump’s tariffs.

But did all of this additional investment help American workers? Hardly. Automotive employment, which had been rising steadily since collapsing during the Great Recession, suddenly began to reverse beginning in 2019 as thousands of jobs were shed monthly. Today, despite a rebound since the pandemic’s abatement, employment in the motor vehicles and parts sectors is still lower than it was in January, 2019. Recent reports coming out of the Philadelphia and New York Federal Reserve Branches both evidence declining manufacturing output as well as falling general activity, new orders, and shipment. Michigan’s unemployment rate increased more than any other state’s this past month, driven in part by declining employment in manufacturing. Volvo recently announced their need to lay off hundreds of workers in Pennsylvania and Maryland because “orders are down amid market uncertainty.” General Motors will be laying off 700 workers in the US and Canada and US steel company, Cleveland-Cliffs has already laid off 1,200 workers in an attempt to mitigate the effects of the Trump administration’s tariffs on steel and auto imports.

Just what this increased foreign investment was used for is hard to say, but one thing is clear: unlike during the 80s, when foreign investors saw opportunity in the US and invested accordingly, it did not help the American worker.

Investment Follows Open Trade

Like almost all of Cass’s insights into history and economics, he finds a kernel of truth and builds an elaborate monstrosity of an argument on top of it relying on revisionist history and fallacious post hoc reasoning. The simple truth is that the VER that Japan negotiated did not lead to increased foreign investment in the United States beyond what was announced years prior to the VER even being considered. In fact, foreign investment in the United States increased dramatically when VER was rescinded, not while it was in effect.

Trade liberalization confers upon the twin benefits of lower prices for consumers and lower costs for producers. The lower prices mean consumers can better afford their purchases, improving their own economic livelihoods. The lower costs for producers (which get passed on to consumers) mean cheaper production in the US relative to other nations. These lower costs attract foreign investment, spurring domestic job growth and increasing wages.

Ronald Reagan’s commitment to free trade is certainly complicated by the VER with Japan. While protectionists like Oren Cass argue that the VER spurred manufacturing job growth and increased foreign investment, the evidence paints a different picture. Short-term gains from the VER were eroded by long-term inefficiencies in the US auto industry as reduced competition stifled innovation. The Big Three automakers failed to adapt to shifting consumer demands for fuel-efficient, reliable cars, which resulted in massive layoffs and plant closures in the 1990s.

To the extent that foreign investment in the US occurred during the VER, it was in fact driven by broader economic factors like cost differentials and exchange rates, not protectionism. Reagan’s commitment to free trade is intact. Likewise, the VER’s legacy underscores a crucial lesson: protectionist measures can deliver short-term gains at the expense of long-term prosperity. Actual economic strength lies in open markets, competition and innovation — values that Reagan championed, even with the VER.