On October 26th, the first calculation of third-quarter US Gross Domestic Product will be released by the Bureau of Economic Analysis. The most recent Bloomberg forecasts show a substantial increase over the second quarter’s 2.1 percent growth. The mean of current projections for tomorrow’s third-quarter GDP release is 3.4 percent, with a median of 3.5 percent, drawn from 73 forecasts ranging from -0.03 percent to 5.4 percent. The Federal Reserve Bank of Atlanta’s GDPNow estimate as of today is 5.4 percent. If realized, the Bloomberg mean estimate would represent a 62 percent jump over the second-quarter reading; the Atlanta Fed’s number, a leap of 157 percent. If the third-quarter GDP number were to come in at 4.5 percent or higher, it would be the highest quarterly return since the late 2020 through 2021 recovery from pandemic policies. Barring that, a quarterly GDP result higher than 4 percent has not been seen since the third quarter of 2019.

More important than historical comparisons, though, would be answers to the following questions: Where in the components of GDP would such strength be coming from, especially considering that Fed rate hikes are beginning to exert a decelerating effect on the US economy? Is it a consequence of policy, or random economic interactions at the micro, meso, and macro levels? And does such a bounce in GDP portend a return to robust economic output, or a capricious, insignificant surge?

It is difficult to say in advance. But several factors behind the estimates for a strong third-quarter number are likely among the index’s constituents. US consumers have continued to buoy the US economy, as evidenced by the strength of discretionary spending on the Barbie and Oppenheimer films, the Taylor Swift and Beyonce’ tours, and vacations. Private inventories have also been rising as well, most recently owing to firms stocking up on supplies in anticipation of broadening labor unrest. The balance of US exports and imports will factor in, but other than a stronger dollar since July 2023 (which drags on US exports while increasing the marketability of imports), those numbers tend to be volatile from one quarter to the next and thus difficult to predict. And private nonresidential fixed investment (which alongside consumption was the other major contributor to the prior GDP release), is likely to play a significant role in tomorrow’s number as taxpayer-provided subsidies from the Bipartisan Infrastructure Law, the Inflation Reduction Act, and the CHIPS and Science Act continue to flow.

If the bottom line third-quarter GDP number shakes out as the Fed’s GDPNow and Bloomberg survey are hinting, and the elements listed above are the cause (consumption, private nonresidential fixed investment, private inventories, and perhaps some help from trade), it is probably not indicative of a renewal of strong economic growth. Other than the three federal spending laws (which are legislatively engineered to disburse government funds at regular intervals, providing an ongoing business spending boost to the US economy through the 2024 election cycle), the remainder of the factors are fickle. Consumers, still spending, have eaten through their pandemic savings, are borrowing at rates not seen in 40 years, and face both contracting credit and the return of student loan payments. The end of federal child care subsidies, and mortgage rates at quarter-century highs are adding to spending headwinds. American consumption has been impressive and somewhat mysterious of late, but cannot continue indefinitely. Accumulated private inventories will either be sold or drawn down once the latest wave of labor activism subsides. Government spending is likely nearly the same from the second to the third quarter and the impact of trade remains to be seen.

Behind all of these questions — if indeed a blowout third quarter US GDP number appears tomorrow morning — is a weightier issue: How will the Fed respond? A strong GDP number is likely to send Treasury bond yields up in anticipation of another rate hike, possibly dragging the 10-year note back above 5 percent. Whatever the specific sources within tomorrow’s GDP, an overall increase by the estimated magnitude is likely to motivate the Fed to intensify its efforts, redoubling its contractionary policy bias.

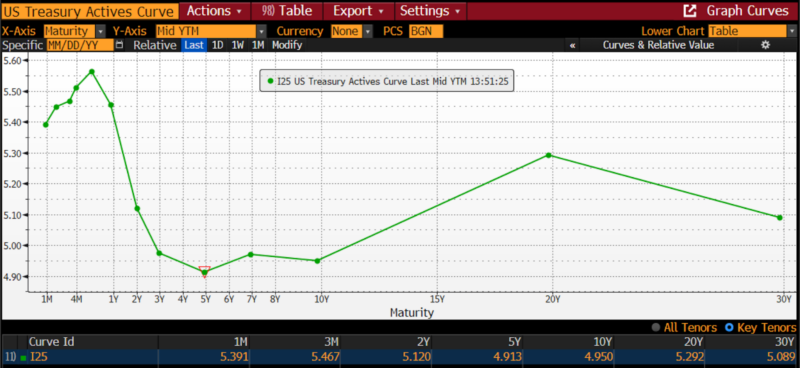

US Treasury Yield Curve, 25 October 2023

Once more, it’s important to note that this is an anticipatory scenario. But if the predicted increase in third-quarter GDP does materialize, and if it is on the order of 4 percent or more, anticipate a continuous promotion and celebration of the economic policies associated with the Biden administration. But aside from offering substantial taxpayer funding for unproven technologies and for ventures without market demand, fostering tensions nationwide between management and labor, raising regulations and taxes, and ramping up both US debt and deficits, the expected growth in GDP won’t be attributable to the economic policies associated with the Biden administration.

One would do well to recall the heroically shameless efforts undertaken by the current administration to distance themselves from two quarters of contracting GDP in 2022. US citizens — consumers, savers, investors, and businesspeople — will, in the event of a strong GDP release on Thursday morning, benefit more from scrutinizing and taking note of any ensuing political self-aggrandizement than by absorbing or even ignoring it. Forthcoming GDP releases may require reminding administration officials of statements made tomorrow regarding the achievements, and prospects, of “Bidenomics.”